- Yield to Maturity

- Posts

- Myth: Small amounts aren’t worth investing.

Myth: Small amounts aren’t worth investing.

Small amounts may be discouraging, but the action is so much more important than the amount.

Clifford Cornell, CFP®

March 06, 2024

There is a famous story that has been told time and again in the field of personal finance. It is so highly covered because it brings about hope for everyone. Couple this with the fact that everyone loves an underdog and you get a tale that never goes stale.

Ronald Read passed away in 2014. He worked as a gas station attendant for nearly 25 years and was also a janitor for about 17 years. Read was said to be a frugal man who enjoyed simple pleasures such as reading and collecting things such as stamps and coins.

Simple life, right? The dude made it, got to retire and enjoy his hobbies. Our friend Ronald Read, the janitor, was worth $8,000,000 at his death. Not because of inheritance, not because he won the lottery but because he was frugal and invested throughout his entire working career.

The average salary for a janitor in 2024 according to salary.com is $34,537. This is significantly lower than the average salary in the United States, which is $59,428. It seems incredible that Ronald was able to amass such a fortune given his income.

Income is the main driver behind wealth. The more you make, the more you have to potentially save. However, income does not necessarily dictate one’s net worth.

Too often, young professionals write off investing because they believe the amount they can invest is negligent. This is NOT TRUE!! Any amount invested when you are young is a considerable amount.

Our minds have an incredibly hard time understanding exponential growth, or compounding. Don’t let this be the reason you stop yourself from investing. When you are young, the action is significantly more important than the amount. Building good habits, such as Ronald did, will be worth their weight in gold down the line.

For 2024, the maximum an individual under 50 may contribute to an account such as a Roth IRA is $7,000.

I have made fun of these types of posts on X, but they do a good job of breaking out what this $7,000 looks like across 12 months.

~$583 per month

~$135 per week

~$19.18 per day

When we break this out, $19.18 per day seems much less daunting, although I completely understand that this may be out of reach for people who are investing in themselves right now. That could be business owners, students, etc.

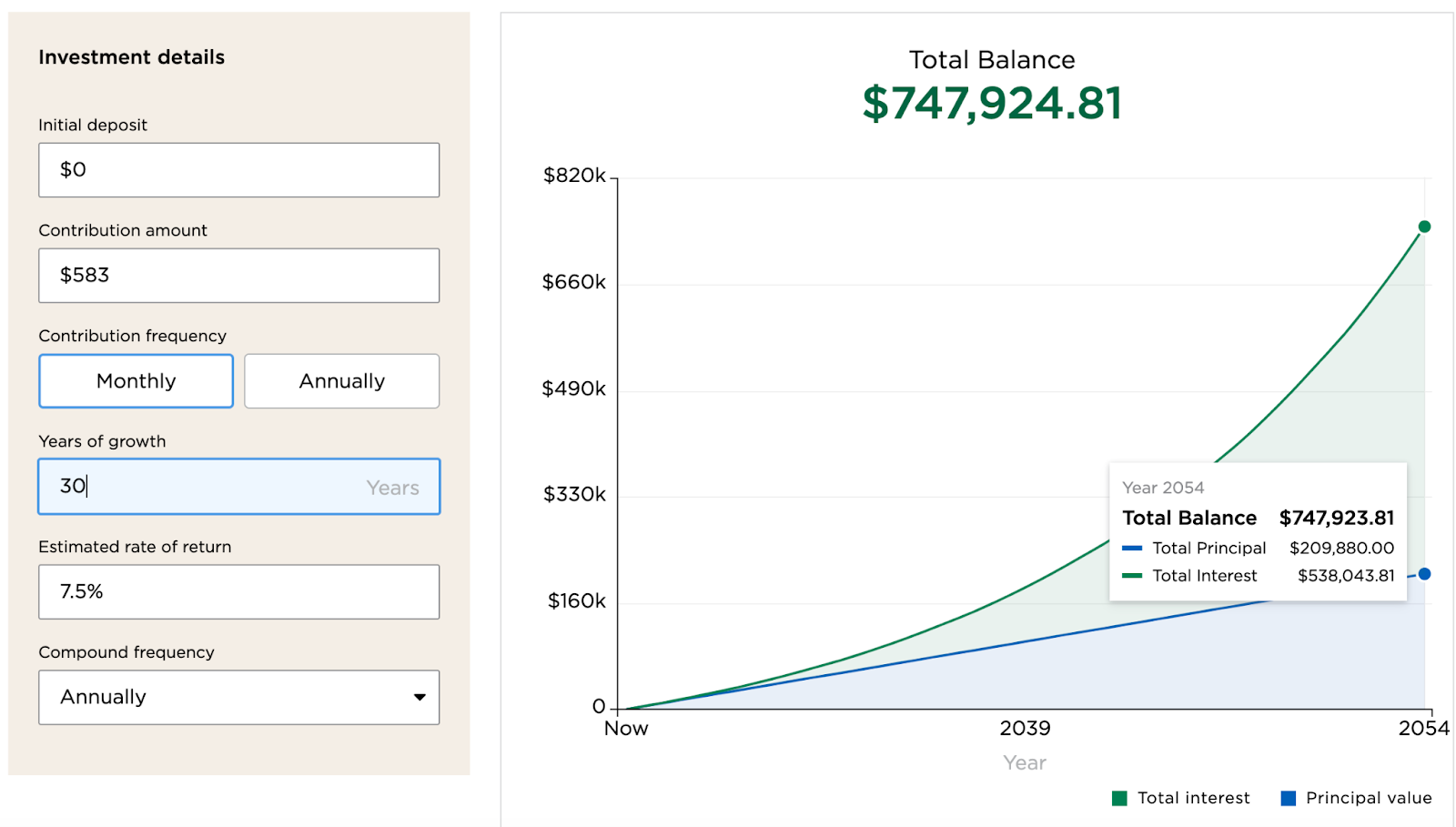

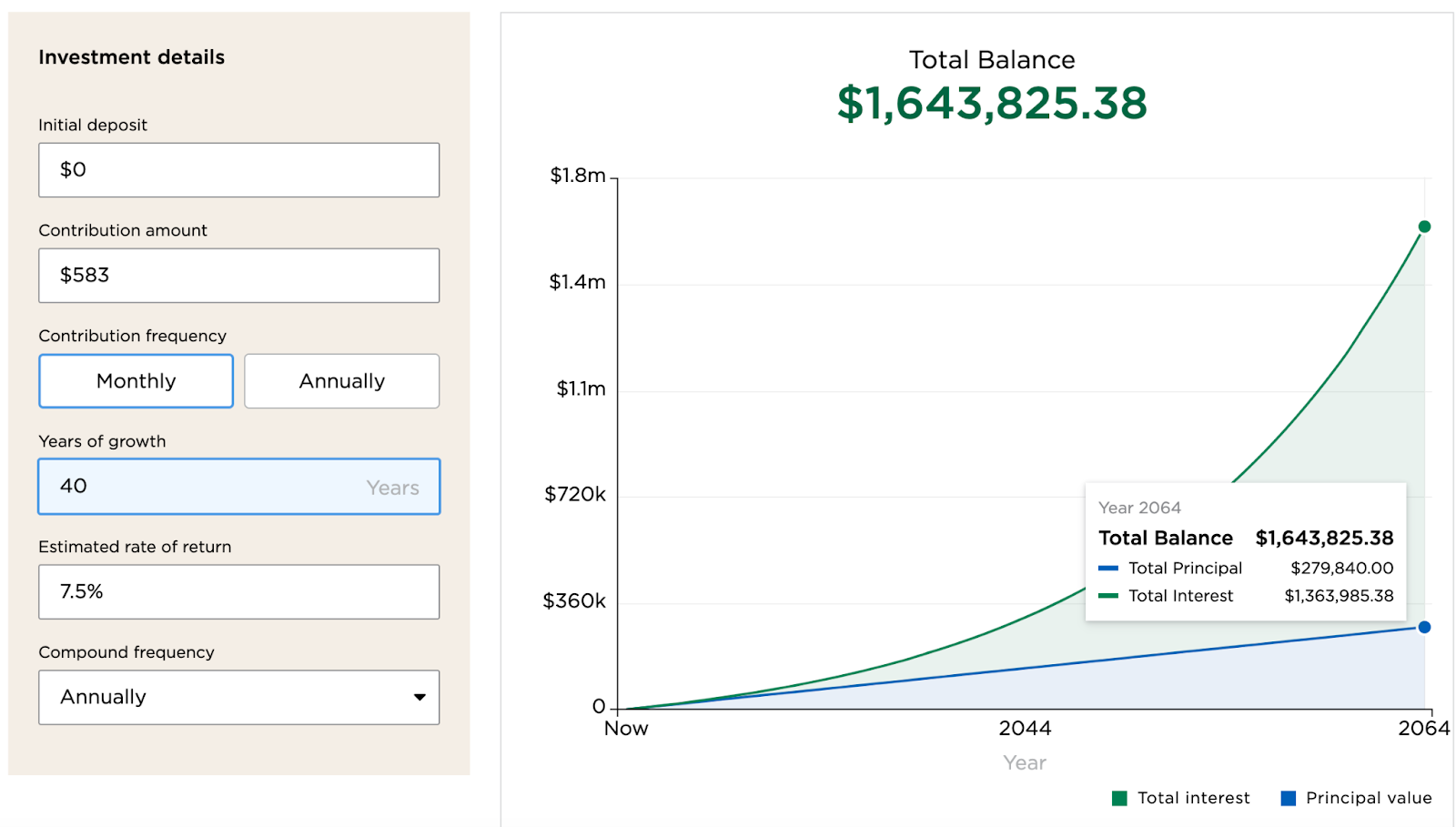

Anyways, let’s see what $7,000 worth of contributions each year can turn into over different periods. We will assume that we contribute $583 monthly.

We will also assume a 7.5% rate of return. (Remember this is annualized over longgg periods of time, not to be expected annually.)

You’ll notice time is your greatest asset when it comes to these calculations. In Scenario 3 we contributed double compared to Scenario 1. However, the additional 20-years worth of compounding makes for a staggering $1.3M increase in total balance.

I want to emphasize that the time you have is the driving factor in these scenarios. The difference between Scenario 1 & 3 is that time doubles, our contributions double, but the total balance quintuples.

These graphs are nothing new to my finance-oriented audience but they might be new for some of the young professionals that are reading. Now $583 per month may be totally out of your ballpark. That is no worry at all. We are young; we have time on our side. Building habits around putting money away is an incredibly valuable skill.

As our income grows, we will already be in the habit of saving and investing. That is where we really start to see the snowball grow.

Do not let the amount discourage you. Taking action is the first step to compounding your wealth. Even small amounts compound over time.

Have a more specific question or want to get your finances in order? Feel free to reach out to [email protected] for a free consultation!